Monoclonal antibodies for Alzheimer’s disease: questionable clinical benefit at a high price

With novel treatments for Alzheimer’s disease dominating the headlines, the most recent being donanemab with the FDA requesting an independent advisory committee to review its safety and efficacy[1], questions remain about their clinical benefit. As the number of patients with Alzheimer’s disease in the US is projected to grow in the coming years, so does the need for a paradigm-changing treatment. However, our model finds that the new monoclonal antibodies offer little clinical innovation over the old standard of care, donepezil. Leaving aside price, their disadvantages in safety/tolerability and dosing outweigh their modest efficacy gains.

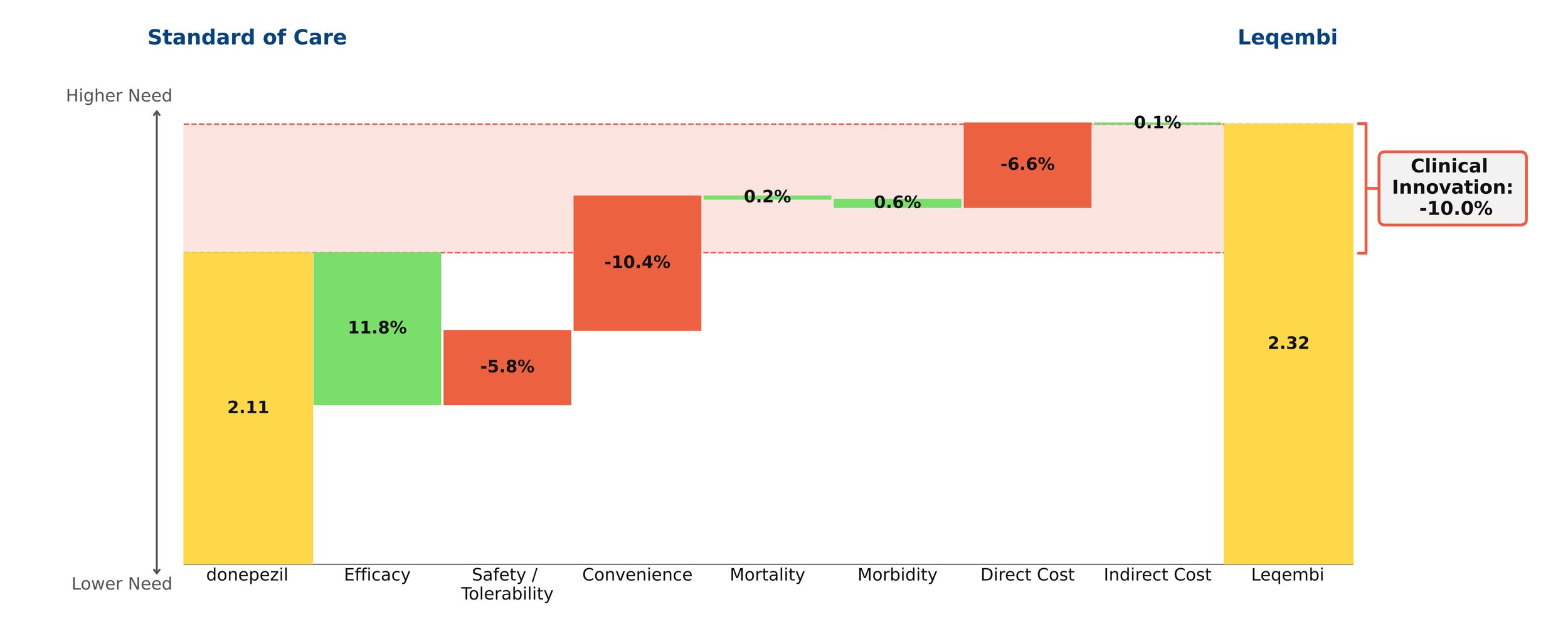

Despite remaining on the market, unlike its ill-fated predecessor Aduhelm, Leqembi shows negative clinical innovation over donepezil of -10.0% in our framework. This is little better than Aduhelm, which shows -11.0% clinical innovation vs. donepezil. As shown above, much of the negative clinical innovation is driven by convenience. Leqembi is given as a one-hour IV infusion every two weeks, compared with donepezil’s once-a-day pill. While Leqembi offers an efficacy benefit measured by standard measures of cognitive decline in AD, this pales in comparison to the inconvenience of the regimen, combined with high cost, high prevalence of potentially serious side effects and a black box warning for amyloid-related imaging abnormalities (ARIA). Questions also remain about how clinically meaningful the improved efficacy is: it is unclear how much patients and their families can appreciate a slowing in cognitive decline of about 6 months for the fraction of patients that experience it.[2]

Even though little separates Leqembi from Aduhelm in our framework, Leqembi has managed to achieve modest sales – around $10.1 million in 2023, still well below the original Eisai projections of $28 million for the year.[3] This is despite the fact that the Institute for Clinical and Economic Review (ICER) deemed its current annual WAC price of around $26,000 to offer low long-term value for money, suggesting a more appropriate price is around $10,000 annually.[4]

In spite of these equivocal results, in-class Eli Lilly drug donanemab was originally expected to be approved this year, with some analysts projecting blockbuster sales of more than $1 billion by 2025.[5] However, our model suggests donanemab will offer slightly lower clinical innovation than Leqembi or Aduhelm, owing to a poorer safety/adverse event profile and higher rates of ARIA.

Leqembi is currently trialing in subcutaneous form, as is donanemab. More convenient dosing would improve the outlook for these agents, but they will still face the headwinds of modest efficacy and significant safety concerns, as well as burdensome monitoring/imaging requirements. With all these considerations, it is difficult to believe that Eisai will hit its revenue target of $8.8 billion by 2032.[6]

[1] Edited to note 3/8/24 New York Times article

[2] https://memory.ucsf.edu/lecanemab

[3] https://www.biopharmadive.com/news/eisai-leqembi-alzheimers-target-revenue-earnings/706668/, https://www.pharmalive.com/eisai-sees-dramatic-increase-in-leqembi-uptake-following-full-fda-approval/, https://www.reuters.com/business/healthcare-pharmaceuticals/eisai-expects-alzheimers-drug-rake-revenue-665-mln-by-march-2023-11-07/

Weighing Efficacy vs. Tolerability: Lenvima + Keytruda in Advanced ccRCC

Conclusion: Despite its toxicity, the overwhelming efficacy advantage of the Keytruda + Lenvima regimen in first-line (1L) treatment of advanced clear cell renal cell carcinoma (ccRCC) puts it in a position to lead the market in this indication. Tolerability concerns will limit its share.

Winning an FDA approval in August 2021, the combination of Lenvima (lenvatinib, Merck + Eisai) and Keytruda (pembrolizumab, Merck) is the most recently approved TKI/IO therapy with an NCCN category 1 recommendation for 1L treatment of advanced ccRCC. This is the third TKI/IO combination to secure an FDA approval and category 1 recommendation, with Inlyta (axitinib, Pfizer) + Keytruda being approved in April 2019, and Cabometyx (cabozantinib, Exelixis) + Opdivo (nivolumab, BMS) approved in January 2021. The approvals and category 1 recommendations of these regimens span all risk groups. These regimens have since bumped sunitinib (Sutent by Pfizer, which went generic in August 2021) from a category 1 recommendation to a category 2A recommendation. Our comparison of the category 1 TKI/IO regimens in this indication shows that although the Lenvima + Keytruda regimen may be more toxic than the others, this disadvantage is modest relative to its major improvement in efficacy. Our analysis is based on phase 3 clinical trial data (CLEAR, CheckMate 9ER, and KEYNOTE-426).

Historically, new regimens with clinical innovation over 10% achieve strong patient share. Lenvima + Keytruda shows 13.4% clinical innovation over Inlyta + Keytruda, driven by improved efficacy.

Lenvima + Keytruda should excel commercially in patients who are able to tolerate it. Dose reductions and interruptions will help manage the toxicity of this regimen and expand its usage to patients who may not able to tolerate it otherwise.

For the clinical benefit that Lenvima + Keytruda provides relative to Inlyta + Keytruda, its higher price is reasonable. Because of this, it falls within the “cloud” of drugs that have historically achieved good market access, and we predict that Lenvima + Keytruda will perform well commercially.

As a side note, Cabometyx + Opdivo is likely to capture share in this indication as a more tolerable alternative to Lenvima + Keytruda, with its efficacy improvement driving its 7.1% clinical innovation over Inlyta + Keytruda.