Conclusion: Pristiq offers no net clinical improvement versus the standard of care — its modest efficacy improvement is offset by its comparable disadvantage in safety/tolerability. This lack of improvement explains its disappointing sales, relative to pre-launch forecasts.

In 2006 senior executives at Wyeth announced that Pristiq (desvenlafaxine) had the potential to exceed $2 billion in peak sales. This forecast included projections for both major depressive disorder (MDD) and vasomotor symptoms (VMS) associated with menopause, an indication for which the drug did not receive approval in the US or EU. In 2012, its fifth year on the market, desvenlafaxine’s global revenue was $630 million, far short of the blockbuster forecast publicized prior to launch. We estimate its patient share in the same year at less than 5% of patients with MDD.

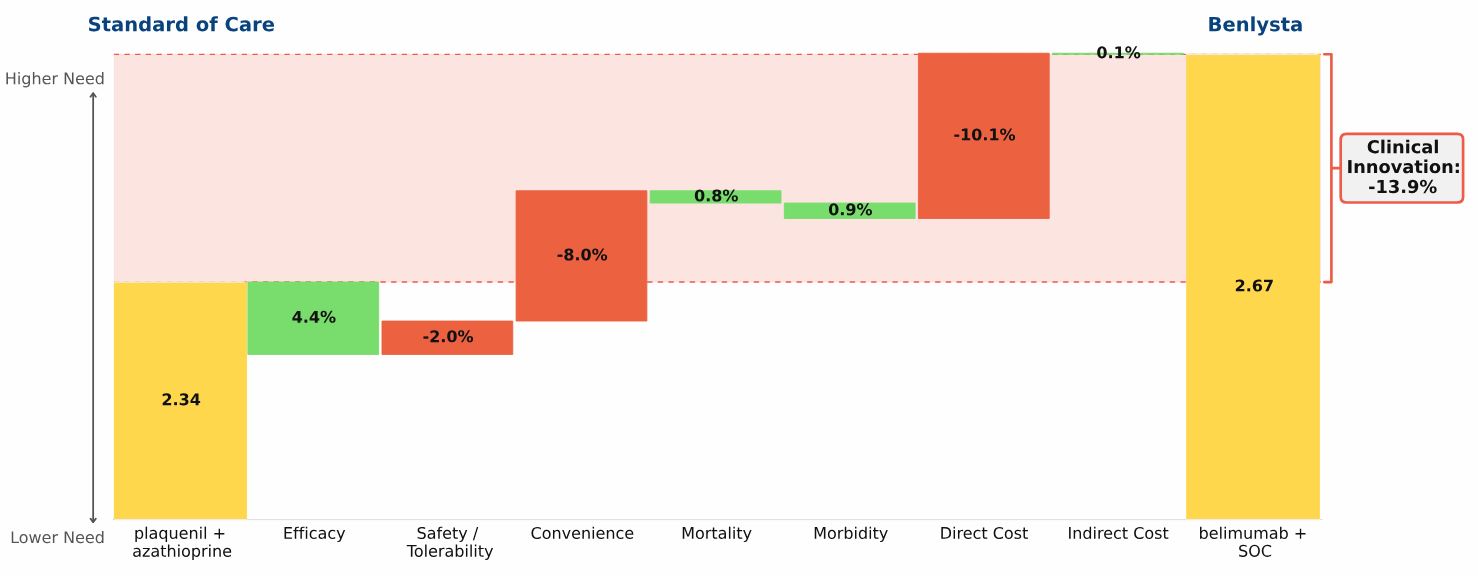

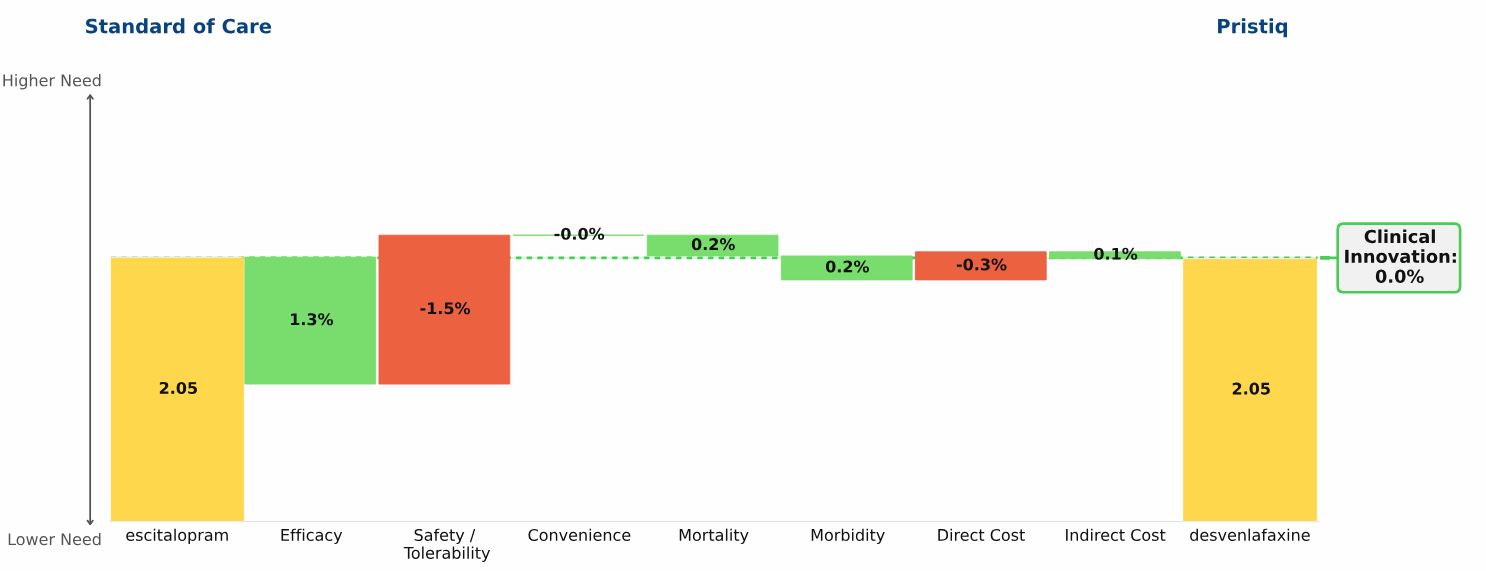

Our Clinical Innovation analysis shows desvenlafaxine to be a “me-too” product, compared with escitalopram (Lexapro) the standard of care (SOC) at the time of launch in 2008.

The “Drivers of Improvement” graphic below illustrates the comparison:

Escitalopram, the yellow bar on the left side of the graphic, and desvenlafaxine, the yellow bar on the right side of the graphic, both have unmet need scores of 2.05

Desvenlafaxine’s Clinical Innovation, or percent reduction in medical need, is therefore 0%: Patients treated with desvenlafaxine have the same unmet need as patients treated with escitalopram

Small differences exist in the two drugs: desvenlafaxine has slightly higher efficacy, slightly worse side effects, and slightly higher cost. For some individual patients, the differences between these drugs will be significant. In aggregate, however, desvenlafaxine does not offer Clinical Innovation over escitalopram, and its commercial performance supports this conclusion.

Given our analysis of lowClinical Innovation for desvenlafaxine, and upon learning that the primary research was reporting a much more favorable commercial outlook, we would have urged the team to reexamine the framing of the trade-offs between the agent’s efficacy and side effects. A second possible source of error is the conversion of the preference share reported by physicians into the predicted patient share — especially in a market as crowded as the depression market.